2018 - What you need to know!

Change is a constant in life and in this industry we are far from immune. 2018 is shaping up as one of big change so what better way to outline what you need to know then via Blog. Whether it's Government Legislation changes, Privacy Protection laws or rates and availability of coverage in the market, 2018 has it all.

We'll start with the one most look at straight away. The total Premium. This is a big one as you will see significant change in this space that may affect your hip pocket. Most Insurers have been absorbing high claim costs for many years mostly through natural disasters. Whatever your stance on Climate Change it is apparent over the past decade that Storm events have much higher impact then in the past and increased levels of severity.

This is a general example but if you times this by the thousands you get a very simple idea of how Insurance works. Insurance commenced as a community pool whereby the losses of the few are covered by the premiums of the many. In principal this hasn't changed one bit. So if after 6 - 7 years of continuous natural disaster claims and no big change in premiums, the pot of cash to pay claims will run out.

Insurers also earn income via investment markets. However, these too have been at records low since the GFC in 2009. So low returns from investments and high claims. This is unsustainable. Most Property Insurers are now seeking between 10% - 20% extra in premium. Its pretty consistent too. Whether you are through an Adviser or direct market, most are seeking these increases to replenish Cash reserves for future claims.

On top of the Insurers seeking additional premium, if you are in NSW you also have the reintroduction of the Emergency Services Levy. (ESL) This is a levy used in part to fund The Fire & Emergency Services in the state. During 2016 - 2017 it was being phased out to zero and was to replaced by a levy on Council rates. This was all set to go until at the 11th hour the State Government did a back flip and advised the change would not go through and a 3 year trial was now in place. All Property Insurers were rolling back the ESL over the 16 - 17 financial year and from January 2017 most had reduced it substantially. It is now back and averaging around 36% of the Base Premium. This then compounds onto the GST and the Stamp Duty. If you have a policy due between May and July this year you need to be ready for bill shock. Last year most Insurer's had reduced the ESL to nil saving you around 30% on the previous year. This year you are set to get a bill with a higher ESL then last year plus a general rate rise. Some renewals in January are already up by 20% - 30% on this time last year so who knows how high this will be come May - June.

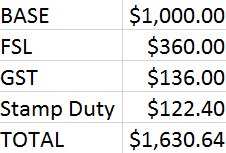

This shows that the Insurance Company only wants $1,000 to cover future claims and their own running costs. You then have an additional $618.40 in Government Charges.

The ESL being removed would make this bill $1,199.00, saving the customer $430 in total taxes and premium. This is now not the case. So if you have a renewal from now up to the end of July you must be aware of these two key changes. Insurers are seeking more premium on Property classes and NSW taxes have increased. It's a double whammy and will mean we spend a lot of time renegotiating your renewals with your current Insurer and the wider market.

Another Legislative change involves Stamp Duty. The NSW State Government has introduced an exemption on Stamp Duty for Small Businesses in particular product classes. Insurance products that may be eligible include:

• Commercial vehicle insurance, for a motor vehicle that is used primarily for business purposes.

• Occupational indemnity insurance (including professional indemnity) covering liability arising out of the provision by a person of professional services or other services (other than medical indemnity cover).

• Product and public liability insurance covering liability for personal injury or property damage occurring in connection with a business or arising out of the products or services of a business.

• Commercial aviation insurance for an aircraft that is used primarily for business purposes.

This is for Businesses turnover less than $2,000,000.

The legislation for this is very complex and we have spent a lot of time pouring over the detail, seeking advice and direction. We strongly suggest you seek advice from an accountant or Business Planner on this. For some clients the saving is as small as $40, however it is better in your pocket. An example I can give is a Professional Indemnity policy for a client with fee income of around $500,000 may save around $200. (General only)

So whilst the Government takes away on one hand they give back part in another. My own view is that this Stamp Duty change has a minimal impact on business and we would have benefitted much more from the removal of the ESL. Not to be though. Be aware of these changes and check your renewal notice when it arrives.

Reforms in NSW CTP have also gone through which may see you get a refund on your premium paid in 2017. This is because CTP Green Slip prices were reduced for most classes of vehicles from 1 December 2017. If you purchased prior to this or renewed you may receive a refund. Details are still coming through but you may get a notice of refund in coming months.

The final change I wanted to highlight is Mandatory Data breach Reporting. This will become mandatory as of February 2018 for all entities required to comply with the Privacy Act 1988. This is one which Small Business must act on swiftly and should be well advanced in preparing its reporting methods. If you haven't sourced information yet and confirmed whether you fall into the criteria you should seek independent advice urgently.

Entities will be required to take all reasonable steps to ensure an assessment is completed within 30 days. If an eligible data breach is confirmed, as soon as practicable they must provide a statement to each of the individuals whose data was breached or who are at risk, including details of the breach and recommendations of the steps individuals should take. A copy of the statement must also be provided to the Office of the Australian Information Commissioner (OAIC). (KPMG 19 May 2017)

The Insurance Landscape changes regularly but usually in manageable ripples. This is the first major shake up I have seen since the GFC in 2009. Moving into what is called a 'Hard Market' in our industry is something we haven't seen in over a decade. You could even say it goes back further to events in the early 2000's when Tort Reform, HIH and the World Trade Centre disaster shone a light on the industry. The changes now are not as radical but all occur at once shaking up the usually benign trading conditions.

For you and I the consumer it means we need to study our renewals closely. Be aware that property premiums are increasing but consider the advice and assistance you are getting before reacting to the bottom line. Our levels of service have gone up even more and we are more active behind the scenes in our negotiations with Insurers for you. You have us on call 24 hours a day to assist with claims management and Risk advice on non insurance matters. We can conduct Cyber, WH&S or Property surveys with our Five Star Benchmarking technology. We can direct you to experts on Contract Review services and be your advocate and voice when a claim occurs.

Here's to a great 2018. I hope the above has helped you understand the current landscape a little better. If ever in doubt, get in touch.

** Information contained is general in its nature. No real individuals own circumstances have been utilised and all examples are general. Please seek your own advice in regard to your own circumstances.

Comments

Post a Comment